Nachrichtenartikel

QIMA 2022 Q4 Barometer

4. Okt. 2022

Q4 2022 Barometer: Eine weitere turbulente Urlaubssaison für Global Sourcing

Nach drei Quartalen im Jahr 2022 zeigen die Daten von QIMA, dass sich die globale Beschaffungslandschaft weiterhin in Bewegung befindet. Die globalen Lieferketten entkoppeln sich immer stärker von China und der Wettbewerb zwischen anderen Beschaffungsmärkten in Asien nimmt zu, während das Schreckgespenst der Rezession im Westen das Verbrauchervertrauen und das Kaufvolumen beeinträchtigt.

Diese Trends in Verbindung mit den anhaltenden Störungen durch Chinas COVID-19-Eindämmungsmaßnahmen, den Naturkatastrophen, die wichtige Rohstoffregionen bedrohen, und den anhaltenden geopolitischen Unruhen deuten darauf hin, dass die globale Beschaffung auf eine weitere turbulente Urlaubssaison zusteuern könnte.

Inflation, Geopolitik und Abriegelungen treiben die Abwanderung der westlichen Käufer aus China weiter voran

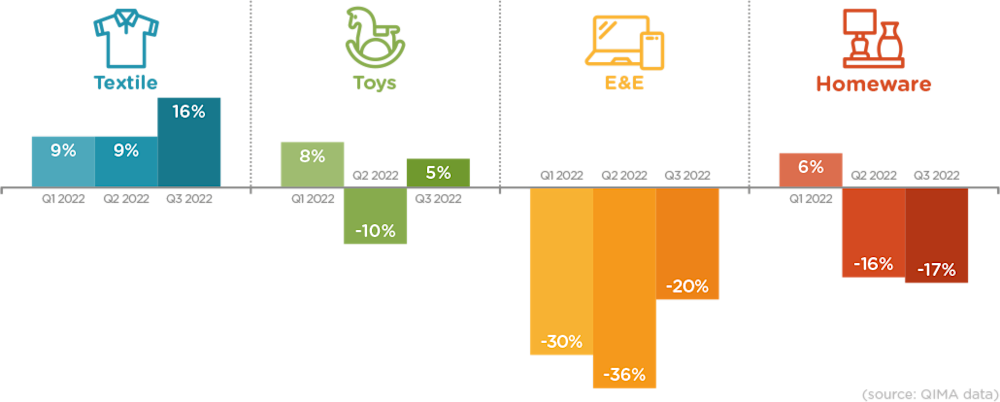

Die QIMA-Daten zur Nachfrage nach Inspektionen und Audits zeigen, dass das Interesse westlicher Einkäufer an der Beschaffung in China im dritten Quartal 2022 im gleichen Tempo wie im ersten Halbjahr 2022 weiter zurückging. Die Nachfrage nach Inspektionen und Audits von Einkäufern aus den USA und der EU ging im dritten Quartal um -5% gegenüber dem Vorjahr zurück, was die durch die Inflation gedämpfte Verbraucherstimmung in den USA und der EU, die fortgesetzte Abkopplung der westlichen Lieferketten von China und die anhaltenden störenden Auswirkungen der COVID-19-Sperren widerspiegelt - trotz früherer Hoffnungen, dass Chinas Übergang zu einer "dynamischen Null-COVID"-Politik die Belastung der Fertigung durch die Vireneindämmung verringern würde. Der Elektro- und Elektroniksektor ist nach wie vor mit am stärksten betroffen, und zwar aufgrund der anhaltenden Halbleiterknappheit und der zunehmenden Verlagerung der Technologiebeschaffung zu Chinas Konkurrenten, darunter Vietnam, Malaysia und neuerdings auch Indien.

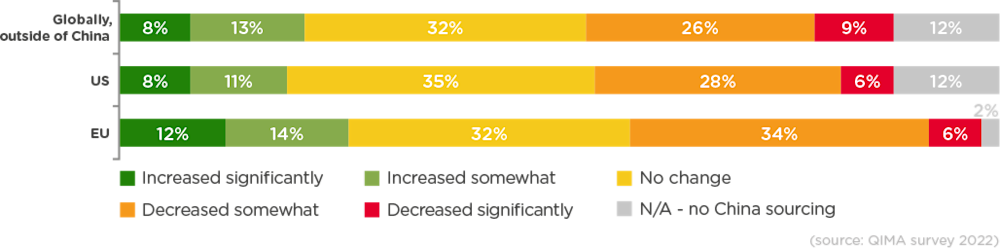

Dennoch bleibt die Abkehr der westlichen Einkäufer von China langsam: Während mehr als zwei Drittel der Befragten der QIMA-Umfrage 2022 angaben, dass sie 2022 nicht mehr bei chinesischen Lieferanten einkauften als 2021, haben nur 6 % ihre Beschaffung in China deutlich reduziert. In einer ähnlichen Gegenüberstellung, die die anhaltende Bedeutung Chinas für westliche Lieferketten veranschaulicht, zeigen die QIMA-Daten zu Inspektionen und Audits, dass Chinas Anteil unter den wichtigsten Beschaffungsmärkten westlicher Einkäufer auf einem Vierjahrestief liegt - aber fast 90 % der in den USA und der EU ansässigen Umfrageteilnehmer nennen China immer noch als einen ihrer TOP-3-Einkaufspartner.

Abb. C1. Von Marken und Einzelhändlern gemeldete Veränderungen des Beschaffungsvolumens in China im Jahr 2022 im Vergleich zu 2021 (Quelle: QIMA-Umfrage)

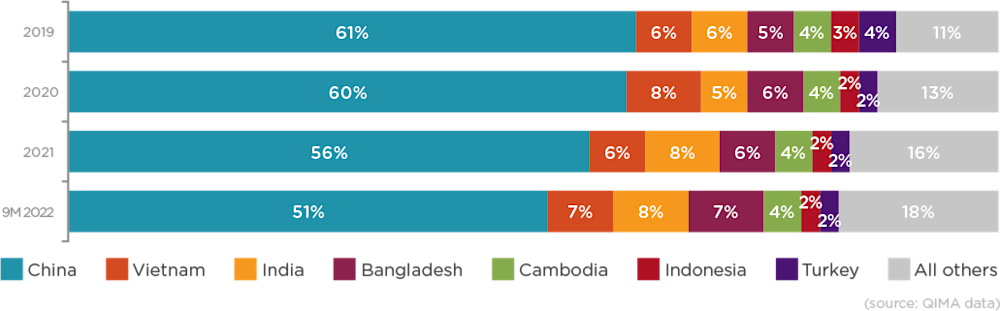

Abb. C2. Die wichtigsten Beschaffungsmärkte der USA und der EU nach Anteil (Quelle: QIMA-Daten)

Abb. C3. Wachstumsdynamik bei Inspektion und Audit in China im Jahr 2022: ausgewählte Branchen (Quelle: QIMA-Daten)

Vietnam ist endlich wieder im Spiel und verwandelt einen zaghaften Aufschwung in ein nachhaltiges Wachstum im dritten Quartal

Nachdem die erste Jahreshälfte 2022 durch Personalknappheit und schwächelnde Nachfrage gedämpft wurde, scheint Vietnam im zweiten Halbjahr 2022 das Vertrauen der Käufer zurückzugewinnen. Nach dem anfänglichen Aufschwung im vietnamesischen verarbeitenden Gewerbe konnte die Dynamik im dritten Quartal erfolgreich in ein anhaltendes Wachstum umgewandelt werden, wobei die Nachfrage nach Inspektionen und Audits von in den USA ansässigen Marken im dritten Quartal um 59 % im Vergleich zum Vorjahr anstieg und sich von EU-Marken mehr als verdoppelte. Die Daten von QIMA zeigen, dass der Zustrom neuer Unternehmen nach Vietnam im August besonders ausgeprägt war und mit einer weiteren Welle von Schließungen in China zusammenfiel.

Abb. V1: Wachstumsdynamik des vietnamesischen Inspektions- und Auditbedarfs im Jahr 2022 (Quelle: QIMA-Daten)

Andere Beschaffungsziele in Südostasien sind ebenfalls gut in das zweite Halbjahr 2022 gestartet. Die Daten von QIMA zeigen eine zweistellige Zunahme der Nachfrage nach Inspektionen und Audits in Indonesien, Thailand und Malaysia über mehrere Produktkategorien hinweg. Insbesondere Malaysia wird zunehmend für die Beschaffung von E&E-Produkten in Betracht gezogen, da globale Technologiemarken Produktionsvolumen aus China verlagern.

Indiens Wachstumstempo stabilisiert sich nach einer Phase der explosiven Expansion

Nach vielen aufeinanderfolgenden Quartalen mit explosionsartigem Wachstum scheint sich die indische Beschaffung auf ein nachhaltigeres Wachstumstempo einzustellen, wobei die Nachfrage nach Inspektionen und Audits in den ersten neun Monaten 2022 um 13 % gestiegen ist (gegenüber einem Wachstum von +41 % in H1 2022). Ein Teil dieser Verlangsamung kann auf die hohe Inflation in der EU und den USA zurückgeführt werden, die die Verbrauchernachfrage nach nicht lebensnotwendigen Gütern wie Bekleidung und insbesondere Haushaltswaren schwächt.

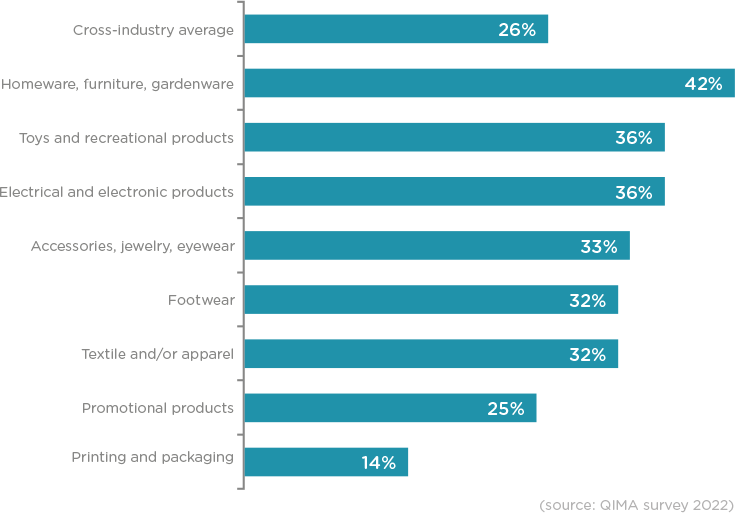

Trotz der Bedeutung dieser Produktkategorien für die indischen Exporte beginnt und endet die Beschaffung in Indien jedoch nicht bei Textilien, wie das zunehmende Interesse großer Elektronikmarken, darunter Apple und Google, an den indischen Produktionskapazitäten zeigt. Die QIMA-Umfrage ergab, dass mehr als ein Drittel der Befragten, die im E&E-Sektor tätig sind, ihre Beschaffungskapazitäten in Indien im Jahr 2022 ausweiten werden.

Andere Länder in der Region haben mit ihren eigenen Herausforderungen zu kämpfen, von der anhaltenden Wirtschaftskrise in Sri Lanka bis hin zu den verheerenden Überschwemmungen in Pakistan, die fast die Hälfte der Baumwollernte des Landes vernichtet haben. Zusammen mit der Verlangsamung der Aufträge aus dem Westen haben all diese Faktoren dazu beigetragen, dass die Inspektion und die Nachfrage in der südasiatischen Region insgesamt vergleichsweise bescheiden um 10 % gestiegen sind.

Abb. I1. Unternehmen, die angaben, ihre Beschaffung in Indien im Jahr 2022 auszubauen - nach Branche (QIMA-Umfrage)

Standortnahe Regionen erfahren anhaltendes Interesse als unterstützende Akteure

Auf dem Weg zu einer diversifizierten Beschaffung bauen westliche Marken und Einzelhändler ihre Beschaffungspräsenz in den jeweiligen Nearshoring-Regionen weiter aus. Im Mittelmeerraum verzeichneten die Türkei und Marokko in den ersten neun Monaten des Jahres 2022 einen Zuwachs von 26 % bzw. 24 % bei den Inspektions- und Auditvolumina von EU-Marken, während auf der anderen Seite des Atlantiks die Nachfrage nach Inspektionen und Audits von Einkäufern aus den USA im gleichen Zeitraum zweistellig zunahm. Dieser Trend bestätigt zwar ihre Rolle als wichtige Komponente der Diversifizierungsstrategie für die Lieferkette, aber die in Near-Shoring-Regionen eingekauften Mengen haben noch einen weiten Weg vor sich, bevor sie die Größenordnung der Beschaffung in Übersee erreichen.

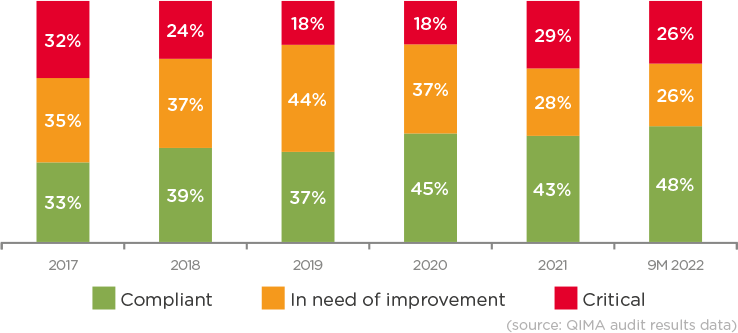

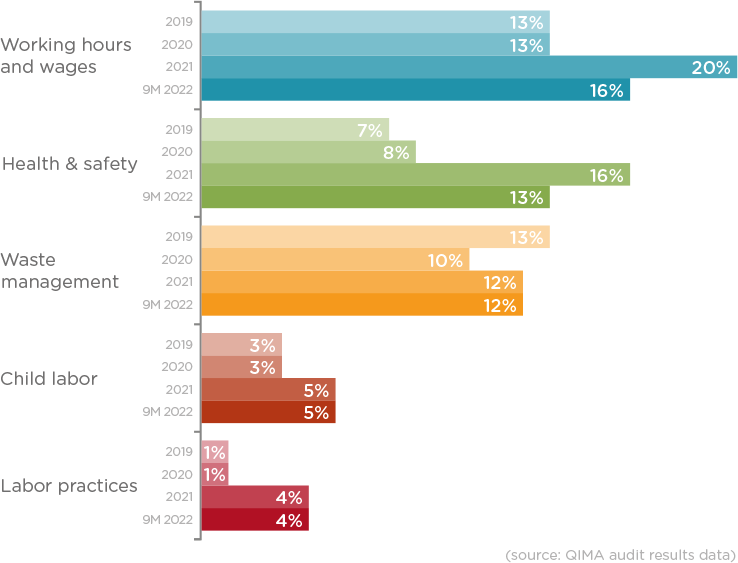

Kritische Verstöße in der Lieferkettenethik übersteigen das Niveau vor der Pandemie

Die von den QIMA-Ethik-Auditoren bei Vor-Ort-Prüfungen im Jahr 2022 gesammelten Daten zeigen, dass sich die Einhaltung ethischer Grundsätze in den Lieferketten noch nicht von der starken Verschlechterung erholt hat, die mit dem Ausbruch der Pandemie einsetzte. In vier der fünf von den QIMA-Auditoren bewerteten Schlüsselbereiche lag der Prozentsatz der Fabriken mit kritischen Verstößen im Jahr 2022 deutlich über dem Niveau von 2019. Alarmierend ist, dass sich die Wahrscheinlichkeit kritischer Verstöße im Zusammenhang mit Kinderarbeit im Jahr 2022 im Vergleich zur Zeit vor der Pandemie fast verdoppelt hat.

Da mehr als die Hälfte der geprüften Fabriken sofortige oder kurzfristige Verbesserungen bei der Einhaltung ethischer Standards benötigen, besteht für Marken und Einzelhändler ein echter Bedarf, mehr Einblick in ihre Lieferketten zu erhalten und konkrete Schritte zu unternehmen, um Verstöße zu beheben - vor allem, wenn man bedenkt, dass die neuen und bevorstehenden Sorgfaltspflichtgesetze in den USA und der EU einen zusätzlichen Anstoß geben.

Abb. E1. Entwicklung der von den QIMA-Ethik-Auditoren vergebenen Fabrik-Rankings, 2017-2022 (Quelle: QIMA-Audit-Ergebnisdaten)

Abb. E2. Prozentsatz der Fabriken mit kritischen Verstößen nach Kategorie, 2019-2022 (Quelle: QIMA-Audit-Ergebnisdaten)

In der derzeitigen unbeständigen Beschaffungslandschaft ist die Flexibilität der Lieferketten gleichbedeutend mit Widerstandsfähigkeit

Die zunehmende Diversifizierung der globalen Lieferketten deutet darauf hin, dass Marken und Einzelhändler auf dem besten Weg sind, die Unsicherheit als neue Norm der globalen Beschaffung zu akzeptieren. Da eine Vielzahl von Störungen in der Lieferkette die globale Beschaffungslandschaft weiterhin erschüttert, werden Unternehmen, die bei ihrer Lieferkettenstrategie auf Flexibilität und Anpassungsfähigkeit setzen, am besten in der Lage sein, die Turbulenzen zu bewältigen.

Presse Kontakt

E-Mail: press@qima.com

Diesen Beitrag teilen