Nachrichtenartikel

QIMA 2021 Q1 Barometer

12. Jan. 2021

Das Jahr 2020 im Rückblick: Die Störung des Welthandels zeigt veränderte Konsumgewohnheiten und hohe ethische Risiken, während die Beschaffung aus China besser abschneidet als erwartet

Fast ein Jahr nach der COVID-19-Krise dominieren Unsicherheit und Störungen weiterhin den globalen Handel. Auch im Jahr 2021 wird die globale Beschaffung weiterhin der Pandemie ausgeliefert sein, was die Bedeutung von Flexibilität und Effizienz in der Lieferkette für das weitere Überleben jedes Unternehmens unterstreicht.

Die QIMA-Daten für 2020 zeichnen ein Bild von zunehmend diversifizierten Lieferketten, sich ändernden Verbrauchergewohnheiten und einer alarmierenden Zunahme ethischer Risiken, die sich in einem Jahr beispielloser Umwälzungen in der globalen Beschaffung abzeichneten.

Schocks auf der Nachfrageseite wirken sich durchweg stärker auf die globale Beschaffung aus als Lockdowns auf der Lieferantenseite

Die QIMA-Daten zur Nachfrage nach Inspektionen und Audits im Jahr 2020 spiegeln die starken Auswirkungen der COVID-19-Sperrungen und Quarantänen auf den Welthandel wider und zeigen deutlich, dass Schocks auf der Nachfrageseite ein größeres Störungspotenzial haben als Sperrungen in angebotsorientierten Regionen. Im ersten Halbjahr 2020 konnten viele westliche Marken und Einzelhändler die Sperrungen in ganz Asien erfolgreich meistern, indem sie die Engpässe bei den Produktionskapazitäten durch die Verlagerung ihrer Beschaffung in Regionen kompensierten, die noch in Betrieb waren (was dazu führte, dass die weltweite Nachfrage nach Inspektionen und Audits im Januar-Februar 2020 nur um 4,5 % im Vergleich zum Vorjahr zurückging). Andererseits führten Sperrungen in den Heimatregionen der Einkäufer immer zu starken Einbrüchen bei der Beschaffung (Nachfrage nach Inspektionen und Audits -31 % im Jahresvergleich im Zeitraum April-Mai 2020) - ein Muster, das sich Ende 2020 mit der Wiedereinführung von Sperrungen in der EU und Teilen der USA wiederholen wird.

Beschaffung in China im Jahr 2020: Vom Nullpatient zur Erholung und Widerstandsfähigkeit

In der ersten Hälfte des Jahres 2020 sah es so aus, als ob China als erstes Land, das von COVID-19 betroffen war, das Epizentrum der Pandemie und die am stärksten betroffene Wirtschaft sein würde. Nach einem katastrophalen ersten Quartal, das durch einen Produktionsstillstand und einen Nachfrageschock gekennzeichnet war, erholte sich die chinesische Beschaffung im restlichen Jahr 2020 langsam aber stetig. Gegen Ende des zweiten Quartals kehrte die Nachfrage nach Inspektionen und Audits in China auf das Niveau von 2019 zurück und wuchs von dort aus in der zweiten Jahreshälfte weiter an, bis sie im Dezember ins Stocken geriet, als in mehreren westlichen Regionen wieder Sperrungen eingeführt wurden. Letztendlich ging das Inspektions- und Auditvolumen in China im Jahr 2020 um 2,8 % gegenüber dem Vorjahr zurück - was trotz der beispiellosen Unterbrechungen einen geringeren Rückgang des Beschaffungsvolumens darstellt als der Rückgang um 3,3 %, der 2019 im Zuge des Zollkriegs zwischen den USA und China beobachtet wurde.

Zumindest teilweise verantwortlich für diese relative Widerstandsfähigkeit war das wiedererwachte Interesse von US-Käufern, die es weniger eilig hatten, China im Jahr 2020 zu verlassen, nachdem sich die Handelsspannungen im Zuge des im Januar 2020 unterzeichneten Handelsabkommens der "Phase Eins" allmählich entspannt hatten. Die Nachfrage nordamerikanischer Marken nach Inspektionen und Audits in China blieb in der zweiten Jahreshälfte 2020 über dem Niveau von 2019, wobei die Nachfrage nach Inspektionen und Audits im Jahr 2020 gegenüber 2019 insgesamt um -3,0 % zurückging, verglichen mit dem starken Rückgang von 2018 auf 2019 um -15 %. Im Gegensatz dazu zeigten die europäischen Einkäufer eine geringere Nachfrage nach traditionellen chinesischen FMCG - dieser Rückgang wurde jedoch durch die boomende Nachfrage nach PSA ausgeglichen, was größtenteils dazu beiträgt, dass die Nachfrage nach Inspektionen und Audits im Jahr 2020 gegenüber dem Vorjahr unverändert blieb und nicht dramatisch zurückging.

Diversifizierung der Beschaffung durch die Pandemie beschleunigt, Asiens Produktionsstandorte sind gefragt

Obwohl China ein besseres Jahr als erwartet verzeichnete, hat die Pandemie den langfristigen Trend der Verlagerung von Einkaufsvolumina auf die regionale Konkurrenz deutlich verstärkt: Die Nachfrage nach Inspektionen und Audits in Südostasien stieg 2020 insgesamt um 19 % (doppelt so hoch wie die Wachstumsrate 2019 gegenüber 2018). Insgesamt verzeichnete diese Region ab Juli einen zweistelligen Anstieg der Nachfrage nach Inspektionen und Audits, der durch Käufer, die sowohl kurz- als auch langfristig nach Alternativen zu China suchen, sowie durch massive Aufträge für PSA begünstigt wurde.

In Südasien verlief die Erholung deutlich langsamer (+2,6 % jährliches Wachstum im Jahr 2020 in der gesamten Region, ein Bruchteil des zweistelligen jährlichen Wachstums, das 2019 im Vergleich zu 2018 verzeichnet wurde), wo sich die Hersteller nur schwer von dem Einbruch im April und Mai erholen konnten, der durch die Kombination aus regionalen Lieferstopps und einer durch Lieferstopps im Westen dezimierten Nachfrage katastrophal war.

Lockdowns und Work-from-Home-Bestellungen lösen Verschiebungen in der Verbrauchernachfrage aus

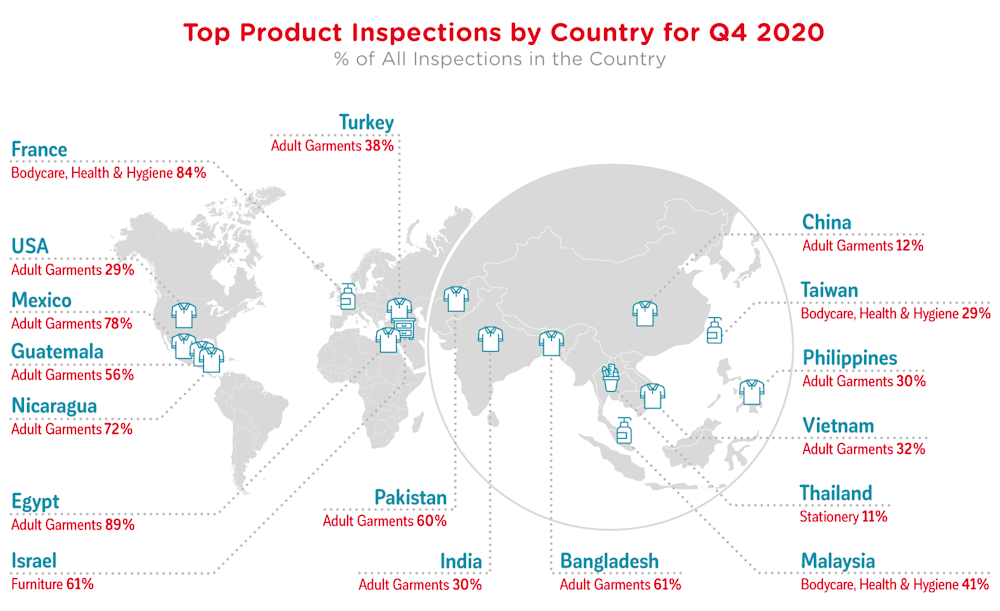

Die aggregierten QIMA-Daten für 2020 zeigen, dass sich die anhaltenden Wellen von Quarantänemaßnahmen und eine noch nie dagewesene Anzahl von Menschen, die im Westen von zu Hause aus arbeiten, bereits in den veränderten Verbrauchergewohnheiten niedergeschlagen haben , was sich wiederum auf die globalen Handelsströme auswirkt. Mit den Modetrends Schritt zu halten und die Garderobe auf den neuesten Stand zu bringen, ist auf der Liste der Verbraucherprioritäten eindeutig nach unten gerutscht, wobei die Nachfrage nach Textil-, Bekleidungs- und Schuhinspektionen bis Ende 2020 weltweit um 11 % gegenüber dem Vorjahr zurückging, nachdem sie seit März - abgesehen von einem kurzen Aufschwung im September und Oktober - auf breiter Front eingebrochen war.

Auf der anderen Seite führten Fernarbeit und Heimunterricht zu einem größeren Bedarf an Kommunikationsgeräten und verschiedenen Home-Entertainment-Produkten. Die Nachfrage der in den USA ansässigen Einzelhändler nach Produkten wie Elektronik und Elektrik, Haushaltswaren und Spielzeug ist im zweiten Halbjahr 2020 sprunghaft angestiegen, wobei alle oben genannten Sektoren das Jahr mit einem zweistelligen Wachstum beendeten: +44% gegenüber dem Vorjahr, +28% gegenüber dem Vorjahr bzw. +46,5% gegenüber dem Vorjahr.

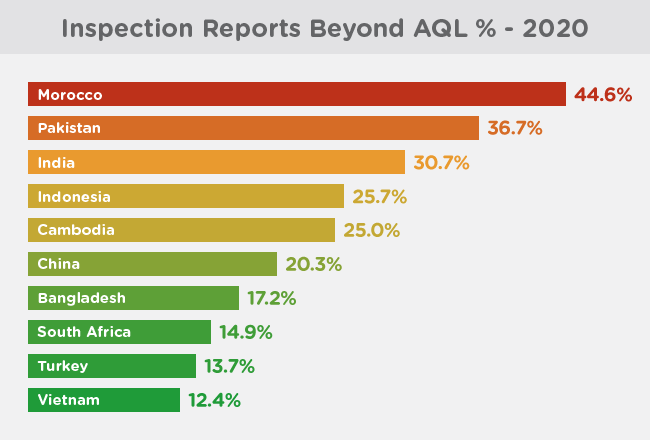

COVID-19 verschärft ethische Risiken in Lieferketten, da Arbeitsrechtsverletzungen sprunghaft ansteigen

Die miteinander verflochtenen Herausforderungen der COVID-19-Pandemie haben die Menschenrechtsrisiken in den globalen Lieferketten stark verschärft. Die Probleme reichen von einer erhöhten Anfälligkeit für moderne Sklaverei und Kinderarbeit (aufgrund des hohen Armutsrisikos durch den massenhaften Verlust von Arbeitsplätzen) bis hin zu Arbeitsverstößen in den Fabriken und einer geringeren Aufmerksamkeit für nicht-virusbedingte Sicherheitsmaßnahmen aufgrund der knappen Ressourcen im Bereich Gesundheit und Sicherheit.

Die von der QIMA in wiedereröffneten Fabriken und im Rahmen von Fernaudits erhobenen Daten zu Ethik-Audits zeichnen ein alarmierendes Bild: Der Prozentsatz der Fabriken, die wegen kritischer Verstöße mit "Rot" bewertet wurden, stieg im zweiten Halbjahr 2020 im Vergleich zum ersten Halbjahr um mehr als 100 %. Einige der drängendsten Probleme liegen im Bereich der Einhaltung von Arbeitszeiten und Löhnen: In China erhielten 14 % der geprüften Fabriken aufgrund von kritischen Verstößen im Bereich der Arbeitszeiten und Löhne die Note "Nicht bestanden". Beispiele für Verstöße sind Sanitärarbeiten, die als unbezahlte Überstunden auferlegt werden, sowie Arbeitnehmer, die zu überlangen Arbeitszeiten gezwungen werden, um die engen Zeitpläne für stark nachgefragte Waren wie PSA einzuhalten.

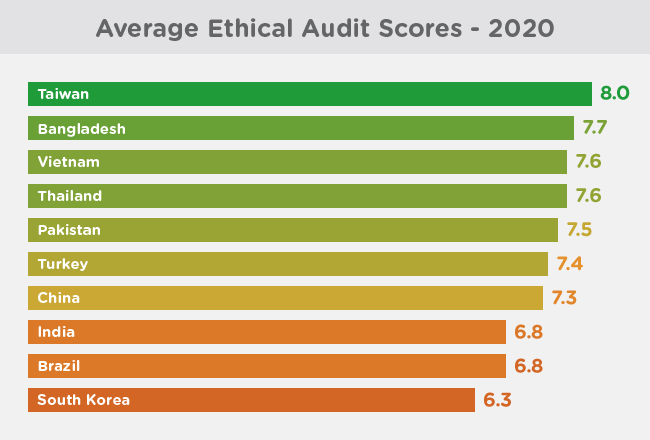

Als Reaktion auf die zunehmenden ethischen Risiken und den eingeschränkten physischen Zugang zu den Fabriken setzen immer mehr Unternehmen auf technologische Lösungen für die Einhaltung der Vorschriften und die Qualitätskontrolle. Dazu gehören Fernaudits, Sprachlösungen für Arbeitnehmer und integrierte Plattformen für die Qualitätskontrolle und die Einhaltung der Vorschriften, die es ihnen ermöglichen, ihr Beschaffungsnetzwerk abzubilden und einen besseren Einblick in die verschiedenen Ebenen der Lieferkette zu erhalten.

QIMA-Barometer Schlüssel-KPIs

Presse Kontakt

E-Mail: press@qima.com

Diesen Beitrag teilen